GOLD

Gold retreated overnight to open at 1292.50/1293.50. It climbed to a high of 1299.50/1300.5 on concerns of tougher sanctions on Russia by the West despite a decline in initial jobless claims in the U.S. The metal then declined to a six-week low of 1292.00/1293.00 on dollar strength and speculation that U.S. interest rates will rise sooner than expected. Thereafter, it consolidated to close the day at 1293.50/1294.50.

Gold ended the session at 1294, closing below the 200 day MA at 1296 as

it approaches the 50% Fibo retracement level (1287.45) of the 2014

rally to mid-March. Subsequent downside levels include the 100 day MA at

1272 and the 61.8% Fibo retracement level at 1262.70. Resistance is

expected at 1308 the March 24th close.

Gold ended the session at 1294, closing below the 200 day MA at 1296 as

it approaches the 50% Fibo retracement level (1287.45) of the 2014

rally to mid-March. Subsequent downside levels include the 100 day MA at

1272 and the 61.8% Fibo retracement level at 1262.70. Resistance is

expected at 1308 the March 24th close.

The Labor Department said the number of people who filed for initial jobless benefits in the U.S. last week declined by 10,000 to a seasonally adjusted 311,000 from the previous week’s revised total of 321,000. Analysts had expected jobless claims to rise by 4,000.

The upbeat data added to hopes that the slowdown in economic activity seen at the start of the year would be temporary.

Also Thursday, the National Association of Realtors said its pending home sales index dropped by a seasonally adjusted 0.8% last month, disappointing expectations for a 0.3% gain.

SILVER

Silver moved lower overnight to open at 19.64/19.69. After a brief high at 19.74/19.79, it declined to a low

of 19.60/19.65, prior to concluding the session at 19.70/19.75.

at 19.64/19.69. After a brief high at 19.74/19.79, it declined to a low

of 19.60/19.65, prior to concluding the session at 19.70/19.75.

Silver closed at 19.73. The bearish trend in silver remains intact as the decline approaches the December 31st low at 18.8266. There are no key support levels ahead of the December 31st low.

The gold silver ratio has formed an engulfing bearish reversal; closing at 65.56, below yesterday’s open despite initially trading on an upswing. The upward sloping resistance trend line from the December and February highs has held, highlighting a challenge to further gains. Looking to the downside, the next key levels of support would be expected at 64.50 and 63.80.

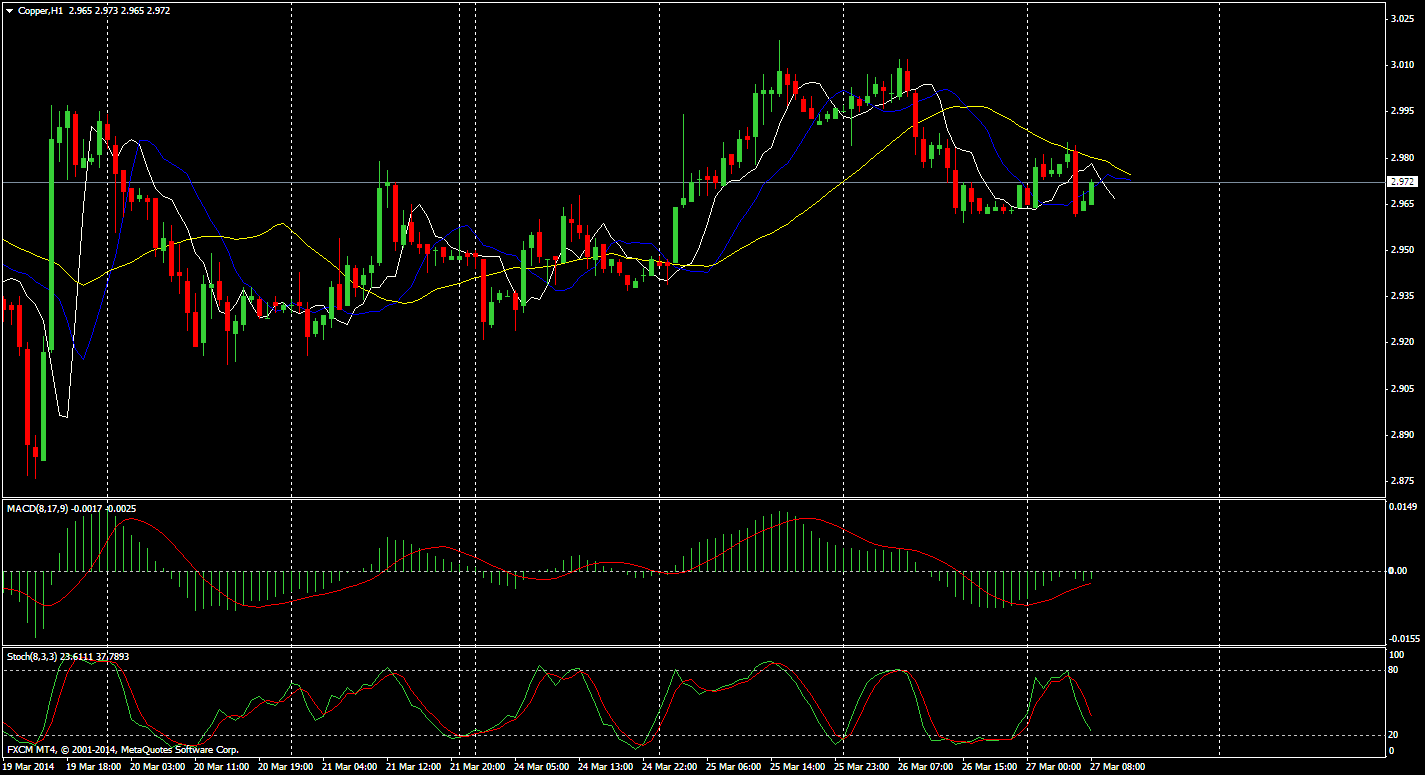

COPPER

On the Comex division of the New York Mercantile Exchange, copper futures for May delivery rose to a session high of $2.986 a pound, before trimming gains to last trade at $2.978 during European morning hours, up 0.4%, or 1.2 cents.

Copper lost 1.33%, or 4.0 cents, on Wednesday to settle at $2.965 a pound.

Futures were likely to find support at $2.939 a pound, the low from March 25 and resistance at $3.045 a pound, the high from March 25.

The U.S. is to publish final data on fourth quarter economic growth, as well as the weekly report on initial jobless claims and private sector data on pending home sales.

Upbeat U.S. durable goods orders figures on Wednesday indicated that economy is gaining momentum in the wake of a weather-induced slowdown.

Meanwhile, in China, data released earlier showed mainland China industrial profits increased 9.4% in the two months through February year-on-year, compared with 17% growth a year earlier.

The industrial metal fell to $2.877 a pound on March 19, the lowest since July 2010, amid growing concerns over the health of China’s economy.

The Asian nation is the world’s largest copper consumer, accounting for almost 40% of world consumption last year.

Copper prices regained strength on Thursday, as investors looked ahead to key U.S. economic data later in the day for further indications on the strength of the economy and the future course of monetary policy..

CRUDE

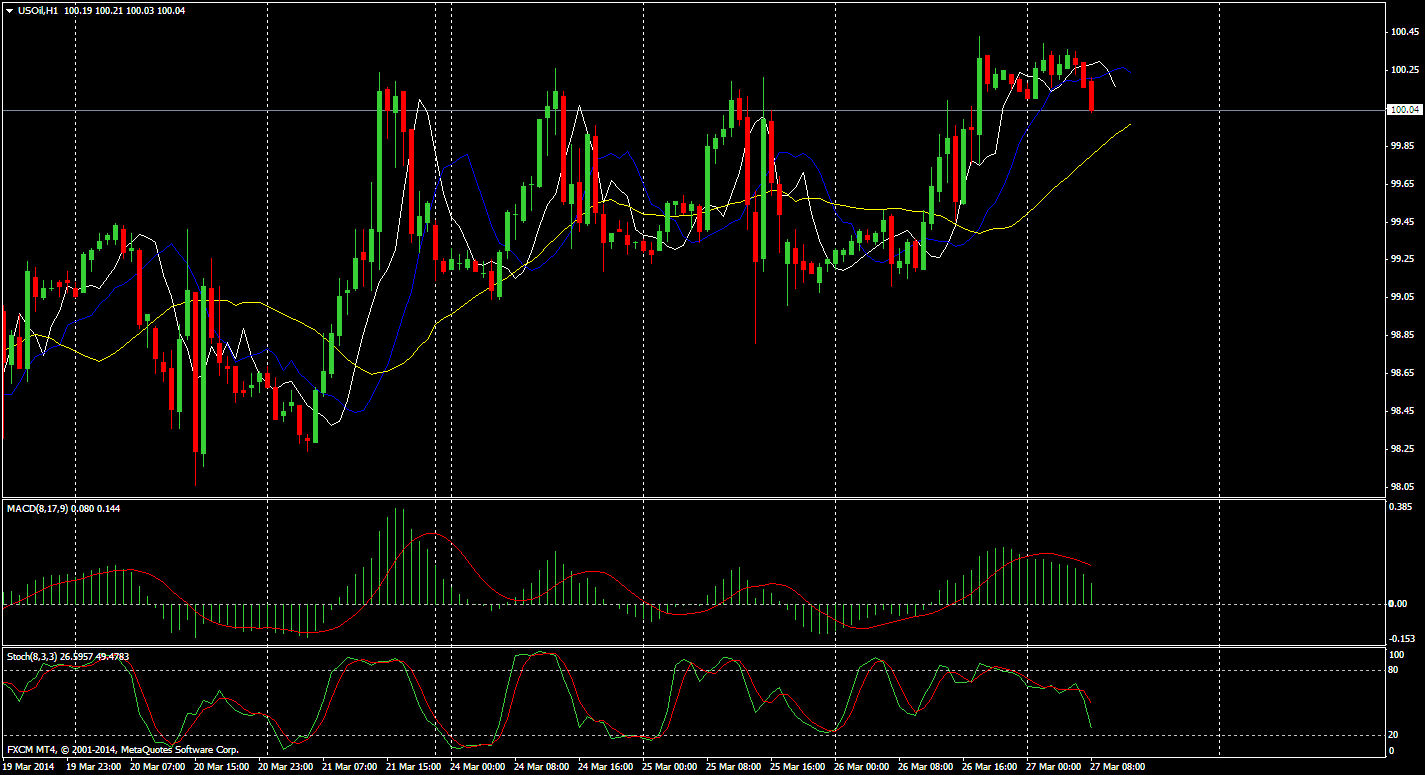

On the New York Mercantile Exchange, West Texas Intermediate crude oil for delivery in May traded at $101.35 a barrel, up 0.07%. On Thursday it reached the highest settlement price since March 7, after hitting an overnight session low of $100.04 a barrel and a high of $101.69 a barrel.

Brent oil on the ICE futures exchange rose 80 cents, or 0.8%, to $107.83 a barrel on Thursday, its highest level since March 14.

Oil prices shot up after the Commerce Department reported earlier that U.S. gross domestic product was revised up to 2.6% in the final three months of 2013, up from a preliminary estimate of 2.4%. Market expectations had been for an upward revision to 2.7%.

Still, the report showed that personal spending was revised up to 3.3% from 2.6% initially, the fastest rate of growth in three years, which drew applause from investors betting that sluggish economic indicators hitting the wire earlier this year were the result of rough winter weather that disrupted commerce and not due to an economic soft patch.

Separately, the Labor Department said the number of individuals filing for initial jobless benefits in the U.S. last week declined by 10,000 to a 311,000 from the previous week’s revised total of 321,000.

Analysts were expecting jobless claims to rise by 4,000.

Also supporting both U.S. and European crude blends were concerns the U.S. and Europe may stiffen sanctions on crude-rich Russia and subsequently threaten global oil supply.

Crude oil prices gained slightly in Asia on Friday on a carryover from overnight better-than-expected U.S. economic growth and weekly jobless claims data.

Technical Levels

Gold retreated overnight to open at 1292.50/1293.50. It climbed to a high of 1299.50/1300.5 on concerns of tougher sanctions on Russia by the West despite a decline in initial jobless claims in the U.S. The metal then declined to a six-week low of 1292.00/1293.00 on dollar strength and speculation that U.S. interest rates will rise sooner than expected. Thereafter, it consolidated to close the day at 1293.50/1294.50.

Gold ended the session at 1294, closing below the 200 day MA at 1296 as

it approaches the 50% Fibo retracement level (1287.45) of the 2014

rally to mid-March. Subsequent downside levels include the 100 day MA at

1272 and the 61.8% Fibo retracement level at 1262.70. Resistance is

expected at 1308 the March 24th close.

Gold ended the session at 1294, closing below the 200 day MA at 1296 as

it approaches the 50% Fibo retracement level (1287.45) of the 2014

rally to mid-March. Subsequent downside levels include the 100 day MA at

1272 and the 61.8% Fibo retracement level at 1262.70. Resistance is

expected at 1308 the March 24th close.The Labor Department said the number of people who filed for initial jobless benefits in the U.S. last week declined by 10,000 to a seasonally adjusted 311,000 from the previous week’s revised total of 321,000. Analysts had expected jobless claims to rise by 4,000.

The upbeat data added to hopes that the slowdown in economic activity seen at the start of the year would be temporary.

Also Thursday, the National Association of Realtors said its pending home sales index dropped by a seasonally adjusted 0.8% last month, disappointing expectations for a 0.3% gain.

SILVER

Silver moved lower overnight to open

at 19.64/19.69. After a brief high at 19.74/19.79, it declined to a low

of 19.60/19.65, prior to concluding the session at 19.70/19.75.

at 19.64/19.69. After a brief high at 19.74/19.79, it declined to a low

of 19.60/19.65, prior to concluding the session at 19.70/19.75.Silver closed at 19.73. The bearish trend in silver remains intact as the decline approaches the December 31st low at 18.8266. There are no key support levels ahead of the December 31st low.

The gold silver ratio has formed an engulfing bearish reversal; closing at 65.56, below yesterday’s open despite initially trading on an upswing. The upward sloping resistance trend line from the December and February highs has held, highlighting a challenge to further gains. Looking to the downside, the next key levels of support would be expected at 64.50 and 63.80.

COPPER

On the Comex division of the New York Mercantile Exchange, copper futures for May delivery rose to a session high of $2.986 a pound, before trimming gains to last trade at $2.978 during European morning hours, up 0.4%, or 1.2 cents.

Copper lost 1.33%, or 4.0 cents, on Wednesday to settle at $2.965 a pound.

Futures were likely to find support at $2.939 a pound, the low from March 25 and resistance at $3.045 a pound, the high from March 25.

The U.S. is to publish final data on fourth quarter economic growth, as well as the weekly report on initial jobless claims and private sector data on pending home sales.

Upbeat U.S. durable goods orders figures on Wednesday indicated that economy is gaining momentum in the wake of a weather-induced slowdown.

Meanwhile, in China, data released earlier showed mainland China industrial profits increased 9.4% in the two months through February year-on-year, compared with 17% growth a year earlier.

The industrial metal fell to $2.877 a pound on March 19, the lowest since July 2010, amid growing concerns over the health of China’s economy.

The Asian nation is the world’s largest copper consumer, accounting for almost 40% of world consumption last year.

Copper prices regained strength on Thursday, as investors looked ahead to key U.S. economic data later in the day for further indications on the strength of the economy and the future course of monetary policy..

CRUDE

On the New York Mercantile Exchange, West Texas Intermediate crude oil for delivery in May traded at $101.35 a barrel, up 0.07%. On Thursday it reached the highest settlement price since March 7, after hitting an overnight session low of $100.04 a barrel and a high of $101.69 a barrel.

Brent oil on the ICE futures exchange rose 80 cents, or 0.8%, to $107.83 a barrel on Thursday, its highest level since March 14.

Oil prices shot up after the Commerce Department reported earlier that U.S. gross domestic product was revised up to 2.6% in the final three months of 2013, up from a preliminary estimate of 2.4%. Market expectations had been for an upward revision to 2.7%.

Still, the report showed that personal spending was revised up to 3.3% from 2.6% initially, the fastest rate of growth in three years, which drew applause from investors betting that sluggish economic indicators hitting the wire earlier this year were the result of rough winter weather that disrupted commerce and not due to an economic soft patch.

Separately, the Labor Department said the number of individuals filing for initial jobless benefits in the U.S. last week declined by 10,000 to a 311,000 from the previous week’s revised total of 321,000.

Analysts were expecting jobless claims to rise by 4,000.

Also supporting both U.S. and European crude blends were concerns the U.S. and Europe may stiffen sanctions on crude-rich Russia and subsequently threaten global oil supply.

Crude oil prices gained slightly in Asia on Friday on a carryover from overnight better-than-expected U.S. economic growth and weekly jobless claims data.

Technical Levels

| SUPPORT 1 | SUPPORT 2 | RESISTANCE 1 | RESISTANCE 2 | |

| GOLD | 1287 | 1279 | 1305 | 1315 |

| SILVER | 19.52 | 19.37 | 19.84 | 20.01 |

| COPPER | 3.0165 | 2.9965 | 3.0465 | 3.0565 |

| CRUDE | 100.30 | 99.33 | 101.97 | 102.67 |

Global Economic Data

| TIME :IST | DATA | PRV | EXP | IMPACT |

| 6.00P.M | Core PCE Price Index m/m | 0.1% | 0.1% | MEDIUM |

| 6.00P.M | Personal Spending m/m | 0.4% | 0.3% | MEDIUM |

| 7.25P.M | Revised UoM Consumer Sentiment | 79.9 | 80.6 | MEDIUM |

| 7.25P.M | Revised UoM Inflation Expectations | 3.2% | LOW |

Core PCE Price Index m/m

| Source | Bureau of Economic Analysis (latest release) |

| Measures | Change in the price of goods and services purchased by consumers, excluding food and energy; |

| Usual Effect | Actual > Forecast = Good for currency; |

| Frequency | Released monthly, about 30 days after the month ends; |

| Next Release | May 1, 2014 |

| FF Notes | Differs from Core CPI in that it only measures goods and services targeted towards and consumed by individuals. Prices are weighted according to total expenditure per item which gives important insights into consumer spending behavior. This is rumored to be the Federal Reserve's favorite inflation measure, but CPI is released about 15 days earlier and tends to garner most of the attention; |

| Acro Expand | Personal Consumption Expenditures (PCE), Consumer Price Index (CPI); |

| Source | Bureau of Economic Analysis (latest release) |

Personal Spending m/m

| Source | Bureau of Economic Analysis (latest release) |

| Measures | Annualized change in the inflation-adjusted value of all goods and services produced by the economy; |

| Usual Effect | Actual > Forecast = Good for currency; |

| Frequency | Released quarterly, about 90 days after the quarter ends; |

| Next Release | Jun 25, 2014 |

| FF Notes | While this is q/q data, it's reported in an annualized format (quarterly change x4). The 'Previous' listed is the 'Actual' from the Preliminary release and therefore the 'History' data will appear unconnected. There are 3 versions of GDP released a month apart - Advance, Preliminary, and Final. The Advance release is the earliest and thus tends to have the most impact; |

| Why Traders Care | It's the broadest measure of economic activity and the primary gauge of the economy's health; |

Revised UoM Consumer Sentiment

| Source | University of Michigan (latest release) |

| Measures | Level of a composite index based on surveyed consumers; |

| Usual Effect | Actual > Forecast = Good for currency; |

| Frequency | Released monthly, usually on the last Friday of the current month; |

| Next Release | Apr 25, 2014 |

| FF Notes | The 'Previous' listed is the 'Actual' from the Preliminary release and therefore the 'History' data will appear unconnected. There are 2 versions of this data released about 15 days apart – Preliminary and Revised. The Preliminary release is the earliest and thus tends to have more impact; |

| Derived Via | Survey of about 500 consumers which asks respondents to rate the relative level of current and future economic conditions; |

| Also Called | Reuters/University of Michigan Consumer Sentiment; |

| Acro Expand | University of Michigan (UoM); |